These TADSummit 2022 reviews are a chance to give all the excellent content deserved attention and add my commentary on its importance. I cover only my ‘Welcome and What happened since we last met? Where is the Programmable Comms market going?’ presentation as the article ended up being quite long and a bit soapboxy (warning controversial opinions, though I do not consider them controversial). Here is the link to the review of the Keynotes, lots more to come.

If you have a sales kick off in the New Year, I can customize a version of this presentation to provide a fun independent presentation across the programmable communication industry. Without all the controversial social commentary 😉

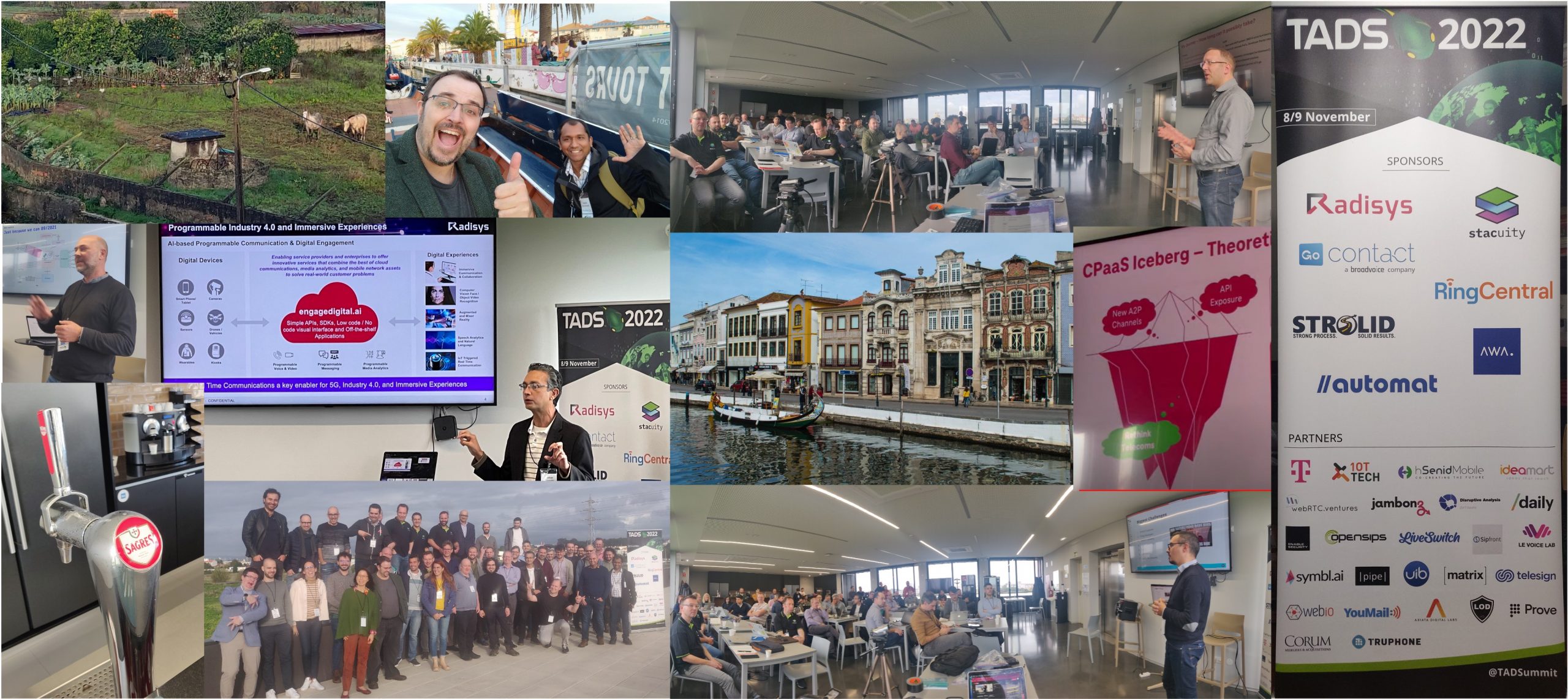

With these links you can get to all the TADSummit content directly: Photos, Videos, Slides, Brief Agenda with videos and slides, Full Agenda with videos and slides.

And I can not say this enough, thank you to STROLID, Broadvoice / GoContact, Radisys, RingCentral, Stacuity, and AWA Network / Automat Berlin for sponsoring TADSummit 2022. And thank you to all the presenters and attendees in making the event excellent.

What happened since we last met? Where is the Programmable Comms market going?

Alan Quayle, independent. Slides & Video.

I had to run through the presentation rather quickly, so I now have a chance to highlight some of the material I skipped over. The pandemic has masked just how intense the past 3 years have been in programmable communications.

In Q1 2020

the discussion was around how can Zoom maintain its current valuation? Growth was without a doubt, but 85% through the rest of 2020 was considered tough. Similarly, for Twilio questions about its continued growth, but Twilio is not a CPaaS, its programmable communications, analysts have it miscategorized. There were only 4 notable M&A transactions, not that untypical before the pandemic. At the end of Q1 2020 the lockdowns began. I was at a Simwood event, and talking with people there on what was about to happen in the UK, as soon as I got home I went to Home Depot and bought a pack of N95 masks that saw me through the pandemic.

The contemporaneous social commentary picture: the bushfires in Australia were the hot issue, more fretting yet general inaction on climate change.

In Q2 2020

Zoom generated 169% year over year revenue growth. Only the previous quarter most people were questioning if 85% was possible. How did Zoom become the default conferencing solution? Freemium, so you could see it was easy to use and just worked, beyond that it was flat monthly / annual fee. Plus they gave it to schools for free, so families started using it. All those nice Web 2.0 principles that the traditional conferencing services had ignored came back to bite them and they could not respond fast enough.

On the M&A front things started to accelerate, Sinch, a global SMS aggregator bought SDI (SAP Digital Interconnect). SAP bought the technology in 2010, with its $5.8bn Sybase acquisition. Sybase itself had purchased the technology, as Mobile 365, back in 2006 for $400m. The business unit makes up to circa €340m ($367m) in revenue for SAP. This enabled Sinch to lower the cost of a big piece of its COGS (Cost of Goods Sold).

There are 5 aggregators with direct connections to the US carriers. The reasons carriers are only able to work with a few aggregators has to do with history and learned incompetence, like most things in telecoms.

The social commentary picture: the murder of George Floyd by a police officer in Minneapolis. And the mass protests around America that followed. I’d never been involved in a protest, however, the political circus of the previous 3 years had even my religious conservative neighbors join the protest.

In Q3 2020

Twilio achieved 132% revenue growth. All those alerts and notifications for touchless pick up, and the explosion of business processes moved onto voice and SMS. RingCentral was on a partnership roll with Unify, Avaya, ALE, and a list of telcos. Most of the old PBX vendors and service providers had given up on their own cloud solutions and moved to RingCentral. There were also some big funding events with Agora raising $350M, Infobip raised $200M, and Payfone (Prove) raised $100M.

The social commentary picture of the explosion in Beirut of ammonium nitrate (fertilizer and often the first bomb making ingredient for many kids) that killed 218 people and injured 7000. The cause was the usual mix of mismanagement of the port, corruption of the government, and inaction of the ship owner. And no one is being held responsible, the investigation has stalled.

In Q4 2020

Bandwidth bought Voxbone, Twilio bought Segment, Five9 bought Inference, Infobip bough Openmarket for $300M (like Sinch bought SDI), SFDC bought Slack, Cisco bought imimobile, etc. As well as a number of big funding rounds. Sinch raised about $390M on new share issue, and Softbank bought a 10% stake for $690M, that’s a total raise of >$1B. I wonder what they are going to do with all that cash?

The social commentary picture is the mRNA mechanism for the COVID vaccine. Done in less than one year, as well as the start of a new branch of medicine based on the mRNA platform.

In Q1 2021

we didn’t need to wait long to find out what Sinch was going to do with over $1B. They spent it on Inteliquent, a voice aggregator (interconnect) focused on the US market. Sinch now covered SMS and voice aggregation in the largest programmable communication market.

Some of the other action included:

- Genesys buys Bold360. A CCaaS adding conversation intelligence.

- Okta buys Auth0. The combination of employee and customer identity management.

- Thinq buys Commio, LCR (Least Cost Routing) expands its voice offer, and later buys Teli to expand into messaging.

- Gamma buys Mission Labs – strong open source competence, necessary for owning its road map and customer experience in the future.

- Twilio invests in Syniverse. Twilio does not want to be tainted by the telco industry. It want to keep that mess at arm’s length. So investing in Syniverse was preferable to buying.

- Twilio also bought ValueFirst. This gave it better access to the India market, where it had struggled to break in. BUT buying a company where people with relationships who’s stock vests and leave with those relationships is tough. A listed company is limited on its business practices.

- Kaleyra bought mGage, which has direct access to the US carriers.

- Link Mobility bought Tismi. Link had been buying companies across Europe for several years. Many were in living dead mode, or trapped by history, that is making money but not enough money to grow. The hope was rolling up would create scale. Later we’ll see what happens as there were many problems to resolve.

- Sangoma buys Star2Star. Another mid-tier UCaaS product.

The social commentary picture shows the first person to receive the COVID vaccine, nurse Sandra Lindsay. She did not become magnetic or any of the other ridiculous claims made by people who should have spent more time studying during their science lessons. I think people should not be allowed to graduate high school and in my more authoritarian moments the right to vote, without significantly more science and statistics knowledge and in particular the ability to apply that knowledge to everyday situations. People are way too easily misled.

In Q2 2021

Sinch raised another $1B! Also:

- Microsoft bought Nuance – partially for is presence in healthcare with voice tech, as well as lots of lucrative telecoms accounts.

- MessageBird bought SparkPost (email which also brings lots of e-commerce workflows) and closed a $1B round!

- Infobip Acquires Anam, an SMS firewall with some interesting anti-fraud monitoring.

- Twilio buys Zipwhip, finally gave up suing them. Zipwhip screwed up 1800SMS.

- IntelePeer Raises $110M in new funding bringing its 18 month total to $170M

- Signalwire raises $30M

The social commentary picture of some of the children associated with the Canadian Indian residential school system where between 3,200 and 6,000 children died, many were buried in unmarked graves. Perhaps this story was overblown in 2021, it appears to pop up in the news every 10-20 years. I think it needs to be impartially investigated and an official conclusion reached, else it will likely do the rounds in the future.

In Q3 2021

Aircall raised $120 Million Series D Funding at $1B valuation, this is a telecom app running on top of Twilio. $1B for an app! The news kept storming in:

- Broadvoice buys GoContact, congrats to Joao and the team. This is a merger between employee and customer communications, like Zoom and Five9, but focused on the mid-market/SMB with little geographic overlap. Its an example of where context rather that category defines whether a merger makes sense.

- Zoom buys Five9 then doesn’t, it really didn’t make that much sense. Zoom is employee communications and Five9 is customer communications. There are few platform or sales synergies yet. Perhaps in a couple of years.

- Element raised $30 Million, congrats to Matthew and Amandine.

- Talkdesk completes Series D fund raise with $10B valuation! Built at a Twilio hackathon and now $10B! We’ve not achieved that at TADHack, yet!

- Mavenir buys Telestax.

- Unifonic closed a $125M Series B round. Programmable comms for the Middle East and Africa.

- TransUnion buys Neustar for $3.1 Billion. Neustar holds a lot of real time data about you and I, which can be used by businesses for insight. More on that topic later.

The social commentary picture shows the 2020 Summer Olympics, held in 2021. Things were finally starting to feel like normality was close around the world. With the exception of China.

In Q4 2021

M&A was still steaming away:

- Sinch Acquires Pathwire for $1.9B, email and the e-commerce workflows. I think at this point some of the deals where a little exuberant.

- Route Mobile buys Masivian for $50 million, which was reasonable, but can Route Mobile stop the inevitable people and deal exits?

- Twilio’s year long decline begins

- Infobip buys Peerless for $200M – like SInch bought Inteliquent.

- Bandwidth down 45%

- Ericsson makes a $6.2B bid for Vonage – which was silly

- Zoom down 20%, as end of COVID begins.

- 8X8 buys Fuze for $250M. This one made little sense, like Ericsson buying Vonage, it was just to show something is happening.

- Genesys raises $580 on $21B valuation!

- MITTO selling tracking services, which was naughty.

- Dialpad nabs $170 million at $2.2B valuation.

The social commentary picture, is a map of social unrest potential, compare the US to Europe? The US insurrection on January 6th was only one month away.

In Q1 2022

investors started to tighten the purse strings as the end of the pandemic was in sight. Things were returning to normal, but remote working remains a thing in non-authoritarian companies:

- Twilio bought Boku, I thought it was about payments and identity verification (Danal), however, it also included silent verification, see this explanation on the Twilio site.

- Sprinklr Enters CCaaS, a great example on the commoditization of customer communication as a social media management company add CCaaS. Sprinklr is a combination of social media marketing, social advertising, content management, collaboration, employee advocacy, customer care, social media research, and social media monitoring.

- EMnify Raises $57M, who presented at TADSummit several years ago.

- RingCentral RISE (channel support) – a package of resources and support to help its many channels sell RingCentral given its experience.

- Clickatell raises $91m for messaging commerce, that is paying for stuff over WhatsApp.

- Radisys Introduces Engage Digital Platform for Service Providers, sponsored TADSummit 2022, and gave a keynote on the platform.

- T-Mobile and AT&T increased their A2P 10DLC rates. Increasing the cost base of all SMS aggregators. Telcos are seeing incorrect A2P SMS market sizes from analysts and getting greedy. I’ll cover this later in the presentation.

- CAMARA – The Telco Global API Alliance – repeating the mistakes of OneAPI, proof an industry can not learn from the past.

- DT Global Carrier have another go at CPaaS – it’s great to see and I’ll keep my fingers crossed.

- Voxist and VXT join WG2’s Marketplace. Working Group 2 has presented at TADSummit over a number of years. And Karel of Voxist / Le Voice Lab is presenting at this year’s TADSummit.

- Sangoma buys NetFortris (Fonality) – more UCaaS aggregation.

The social commentary picture is the invasion of the Ukraine. An unjustified attack on an emerging democracy causing massive human suffering. Those defending the attack, repeating propaganda as fact, or voting against funding to help the country defend itself should live in infamy.

In Q2 2022

the continuation of remote working caused some respite for investors, and there are still a few big investments.

- Commify enters US market with the acquisition of CDYNE, it’s a business messaging roll-up.

- Stacuity (TADSummit sponsor) and JT IoT partner (global cellular IoT connectivity and carrier neutral IoT platform provider), covered in CXTech Week 16 2022.

- TeleSign introduces Age Verification in the UK, covered in CXTech Week 16 2022.

- Uniphore (conversation automation) raises $400 million at a $2.5 billion valuation.

- MobiledgeX acquired by Google, mobile edge compute was massively overstated. I remember arguing about the potential and being told no one knows the future, so just believe. They needed to have studied math and science harder to see belief generally doesn’t change the real world.

- Sipfront secures angel funding and presents at TADSummit 🙂

- Link Mobility: history finally catches up with them. In CXTech Week 19 2022 I covered the drop from 60 to 12, for the passed few months its been between 6 and 7 NOK.

- Twilio Invests $750m in Syniverse, to control a critical element of its cost of good sold.

- JPMorgan fined £160m for brokers using WhatsApp. History repeats itself, in the past it was AOL IM.

- Nokia’s Cloud Native Communication Suite – its IMS in a box.

- Daily buys Confrere, some of the the people who founded the video conferencing startup appear.in back in 2001. 10 years before Zoom was founded.

- Webio Raised $4M, and presented at TADSummit 🙂

- Aircall becomes a Centaur, Exceeds $100 Million ARR (Annual Recurring Revenue).

The social commentary picture is the first image of a black hole, using Event Horizon Telescope observations of the center of the galaxy M87. Science is wonderful.

In Q3 2022

things are now getting back to normal (China excepted):

- 60 million people in the Matrix – it’s great to see the growth.

- Zoom has 3 million UC Customers – Zoom is now a significant UCaaS provider.

- Sinch restated Q2 costs – the SMS aggregation business can be a little dodgy.

- Avaya: Guidance Down 20% on Revenue / 66% on EBITDA. Enterprises moved away from the legacy contact centers and PBX as they discovered UCaaS and CCaaS work reliably and are much cheaper.

- Scientific American: The Robocalls Problem Is So Bad That

the FCC Actually Did Something. You know the FCC is inept when even the Scientific American points it out! Compared to Europe, the lack of broadband competition, the crazy high mobile prices are all down to a political system controlled by vested interests, and not acting on the best interests of the American people. - Avaya’s and Twilio’s Layoffs. Avaya was not a surprise given the revenue restatement. Twilio also was not a surprise given the need to control its costs and attempt to move the culture back to JFDI.

- Hey Sinch and Infobip! Where’s your Revenue? Sinch and Infobip are the dominant SMS aggregators and their combined SMS aggregation revenues are only $2B. That does not make a $100B market according to Insight Partners

It reminds me of the saying, ‘there are lies, damned lies, and statistics.’ Most of these market reports are rehashed broken analysis. They make money from people buying the report because there’s a big market number, see $100B above. I then go into a rant showing other weak results, where keeping paying clients happy matters more than truth. I recommend people believe their people and customers above analysts.

The social commentary picture is how the drought impacted the UK, partially linked to global warming.

In Q4 2022

chickens were coming home to roost as Softbank sold its stake in Sinch at a fraction of its investment. The first release of the vCon IETF Internet-Draft became available. I reviewed Thomas’s vCon keynote in this article. And Twilio announced the closure of Zipwhip, first sue, then buy, then closedown.

The social commentary picture is of Hurricane Ian, according to DeSantis (the governor of Florida) a once in 500 year event, and he’s a potential US presidential candidate. In the past 5 years 2 category 4 (same strength as hurricane Ian) and 1 category 5 hurricanes have hit Florida. In part I blame the American education system with its focus on English language skills, which are great at creating lawyers / politicians, but America has too many of both. I could rant for ages on this one given my first hand experiences of the US education system. I long for national standard exams of my youth of O, A and S levels, which provided incontrovertible proof of a person’s academic abilities. Rather than someone’s opinion.

On where programmable communications is going, insights from communications data will grow in importance. That is dashboards (improving operations that run on programmable comms); Identity and Data Cleanliness (Twilio’s Segment); and vCon (robot food and insight).

I did say the the social commentary would include controversial opinions, hopefully you enjoyed them or at least found them insightful if you disagree with them. The pandemic was a great leap forward in programmable communications. Now back to a slower rate of change 😉

With these links you can get to all the TADSummit content directly: Photos, Videos, Slides, Brief Agenda with videos and slides, Full Agenda with videos and slides.

And I can not say this enough, thank you to STROLID, Broadvoice / GoContact, Radisys, RingCentral, Stacuity, and AWA Network / Automat Berlin for sponsoring TADSummit 2022. And thank you to all the presenters and attendees in making the event excellent.

4 thoughts on “Welcome & What Happened? Review”

Comments are closed.